When I first looked into buying a house, I assumed I needed a massive pile of cash. Then I discovered the USDA loan, one of the best zero-down-payment options available for low-to-moderate-income families buying in rural and suburban areas.

But figuring out if you qualify can feel like solving a complex puzzle. From strict income caps to hyper-specific eligible locations, the rules are rigid. Luckily, you don't have to guess. You can use Zeitro Strata AI to instantly and accurately verify your mortgage eligibility. In this guide, I'll walk you through exactly what this program is, how it works, and how to get approved.

What Does USDA Stand for?

USDA stands for the United States Department of Agriculture. You might wonder why an agriculture department handles mortgages. It's simple: their core mission here is to boost economic growth and improve the quality of life in rural and suburban communities. By backing these mortgages, the government encourages people to settle outside of heavily populated, expensive urban centers.

What is a USDA Loan?

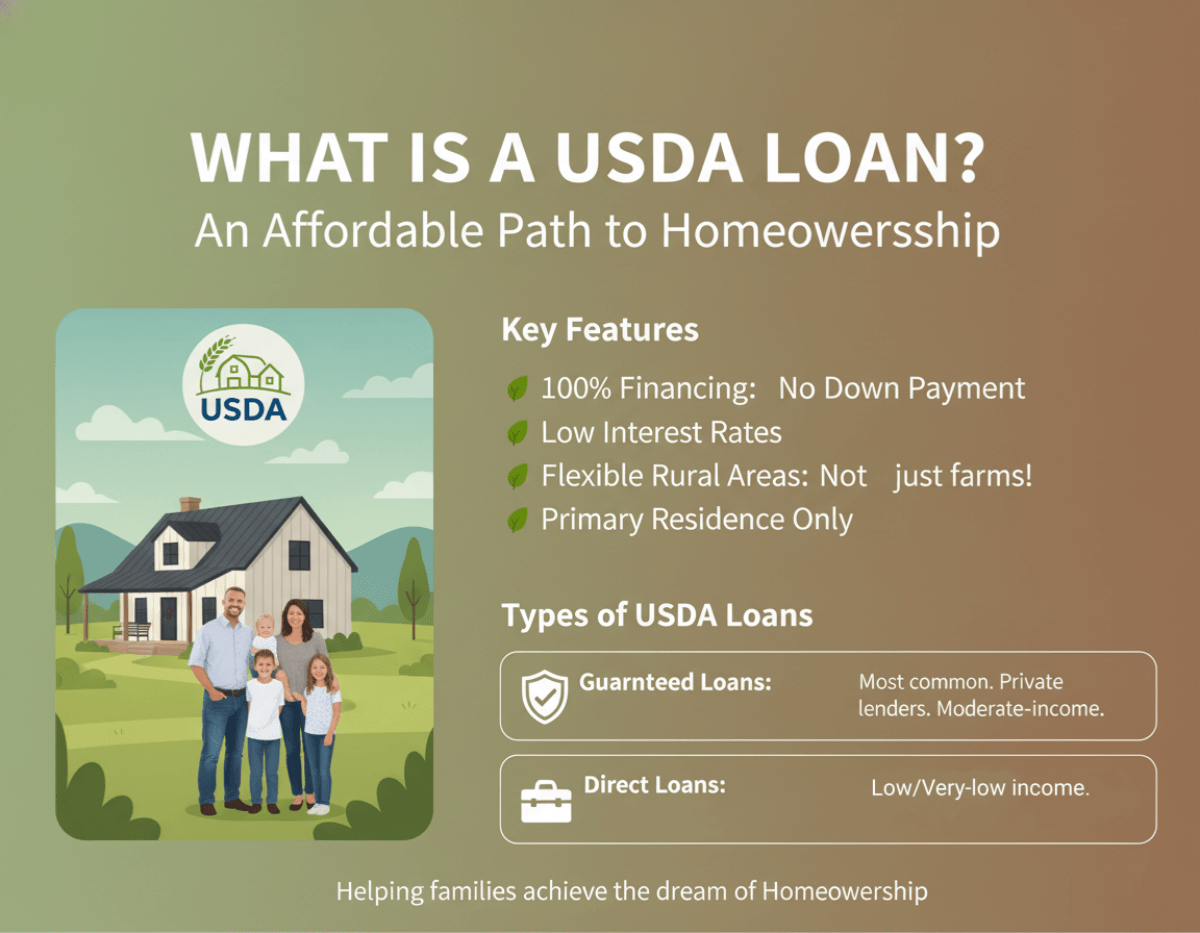

A USDA loan (often referred to as the Section 502 loan program) is a government-backed mortgage designed to help lower- and moderate-income Americans buy homes. Because the government insures a portion of the borrowed amount, private lenders feel completely safe offering 100% financing. That means you can buy a house without putting a single penny down.

When I talk to prospective buyers, their biggest misconception is thinking "rural" means buying a working farm or living miles from civilization. That's simply not true! Many quiet suburbs, small towns, and developments just outside major cities easily qualify. It's an incredible tool for ordinary families who want an affordable path to homeownership without draining their savings accounts.

Types of USDA Loans

Not all of these mortgages are exactly the same. Depending on your financial situation, you'll typically look at three distinct options:

- USDA Guaranteed Loans: This is the most common type. Private lenders issue the funds, and the government guarantees them. It's built for moderate-income buyers who want zero down payment.

- USDA Direct Loans: Issued directly by the government rather than a bank. This version is strictly for low- and very-low-income applicants who cannot secure traditional financing anywhere else.

- USDA Home Improvement Loans and Grants: Need a new roof or structural fixes? These funds help homeowners, especially elderly individuals, repair, upgrade, or modernize their existing properties to remove health and safety hazards.

Features of USDA Loans

What makes this mortgage so attractive? Here are the standout features I always highlight to homebuyers:

- No Down Payment: You get true 100% financing, keeping your savings intact.

- Competitive Interest Rates: Because of the government backing, lenders can offer slightly lower rates than conventional loans.

- Upfront Guarantee Fees: 1% of the loan amount, which can be financed into the loan.

- Annual Guarantee Fee: 0.35% of the remaining principal balance, paid monthly as part of the mortgage payment.

- Primary Residence Only: You cannot use this program to buy a vacation cabin, a rental duplex, or an investment property. You must live in the house.

How Does a USDA Loan Work?

The way this system works is remarkably straightforward once you look under the hood. For the popular Guaranteed program, the government doesn't actually lend you the cash. Instead, the USDA provides a 90% loan note guarantee to approved lenders, covering up to 90% of the guaranteed portion of the loan in case of default.

Because the bank has this massive safety net, their risk drops dramatically. That reduced risk is exactly why they are willing to hand over a mortgage with zero down payment and a low interest rate to someone whose credit score might not be perfect. The lender provides the capital, the government provides the insurance, and you get the keys to your new home.

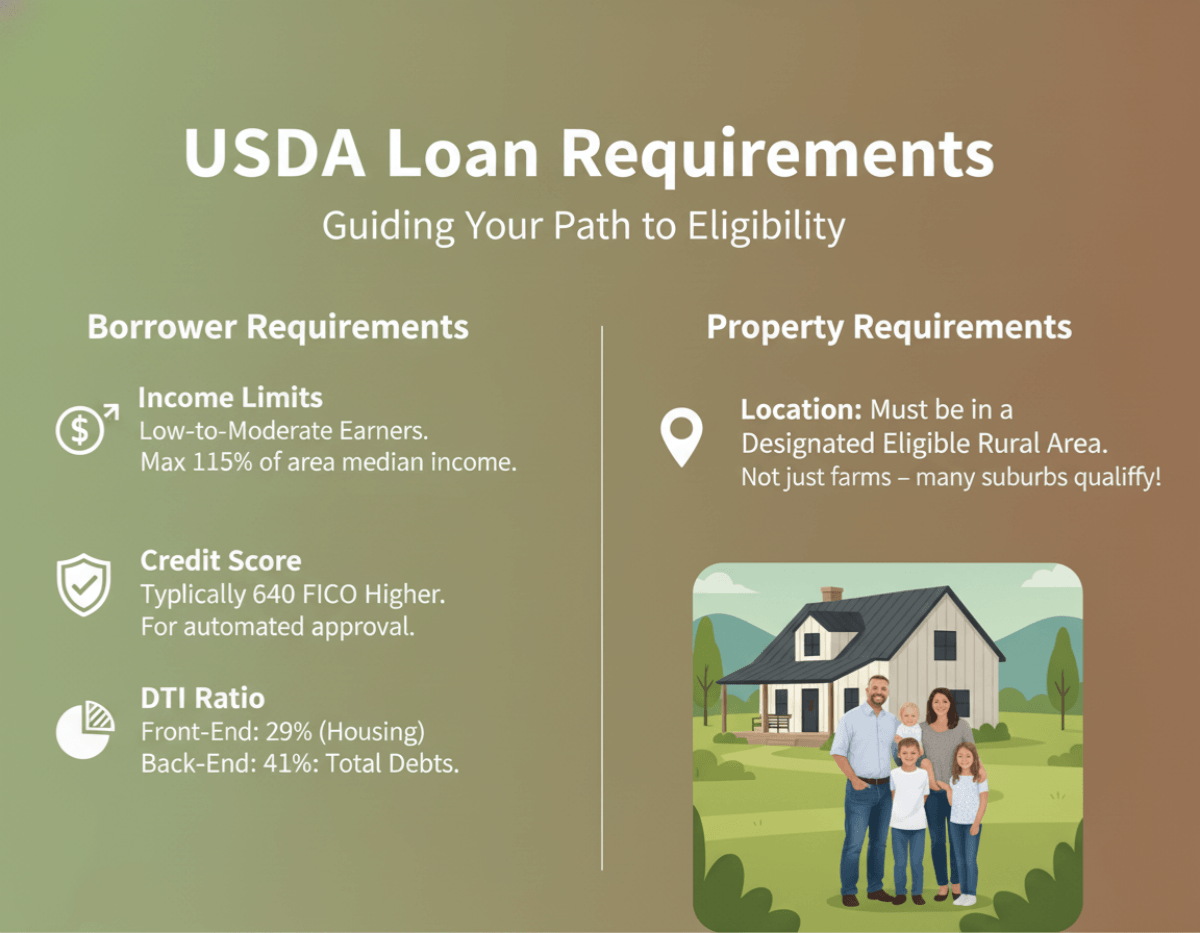

USDA Loan Requirements

To get approved for a USDA loan, you have to meet strict guidelines covering both your personal financial profile and the physical property.

- Income Limits: This program is strictly for low-to-moderate earners. Your total household income cannot exceed 115% of the area's median income. For 2026, standard limits generally sit at $119,850 for a family of 1-4, and $158,250 for 5-8 members. Keep in mind, this includes the income of everyone living in the house, even if they aren't on the actual mortgage application.

- Credit Score: While the government doesn't set a hard minimum, most private lenders look for a 640 FICO score to run your file through automated approval systems.

- DTI Ratio: USDA has no strict official DTI limits, but lenders typically prefer a front-end ratio of 29% (housing costs) and back-end ratio of 41% (total debts). Higher ratios may be approved with compensating factors. That means no more than 29% of your gross monthly income goes toward housing, and 41% toward total debts.

- Location: The house must sit within a designated eligible rural or suburban zone.

Pros and Cons of USDA Loans

Every mortgage product has trade-offs. To give you a realistic picture, here is an objective look at the advantages and disadvantages.

Pros

- Zero Down Payment: Keep your cash in the bank for emergencies, moving costs, or new furniture.

- Cheaper Mortgage Insurance: The 0.35% annual fee is usually much lower than standard FHA mortgage insurance or conventional PMI.

- Competitive Rates: Enjoy lower interest rates thanks to federal backing.

Cons

- Strict Income Caps: If you get a big promotion or raise, you might suddenly make too much money to qualify.

- Geographic Restrictions: You absolutely cannot buy a house in major metropolitan centers.

- Slower Closing Times: Because both the lender and the government have to sign off on the file, the underwriting process can occasionally take longer.

How to Get a USDA Loan?

Ready to move forward? The application process takes a little patience, but following these practical steps will keep you on track:

Step 1: Check your eligibility. Before falling in love with a house, confirm your income and target geography align with the rules. Again, plug your numbers into Zeitro Strata AI for a fast, accurate assessment.

Step 2: Find an approved lender. Not every bank offers these mortgages. Look for lenders who specialize in government-backed rural loans using Bluerate AI Agent so they can navigate the specific paperwork efficiently.

Step 3: Get pre-approved. Your lender will pull your credit, review your W-2s, and give you a pre-approval letter. This tells you your maximum purchase budget.

Step 4: Find a qualified property. Work with a real estate agent who understands the mapping restrictions to find a home that meets the safety and location standards.

Step 5: Apply and close. Once your offer is accepted, your lender finalizes the underwriting. After the federal office gives the final thumbs-up, you sign the papers and get the keys!

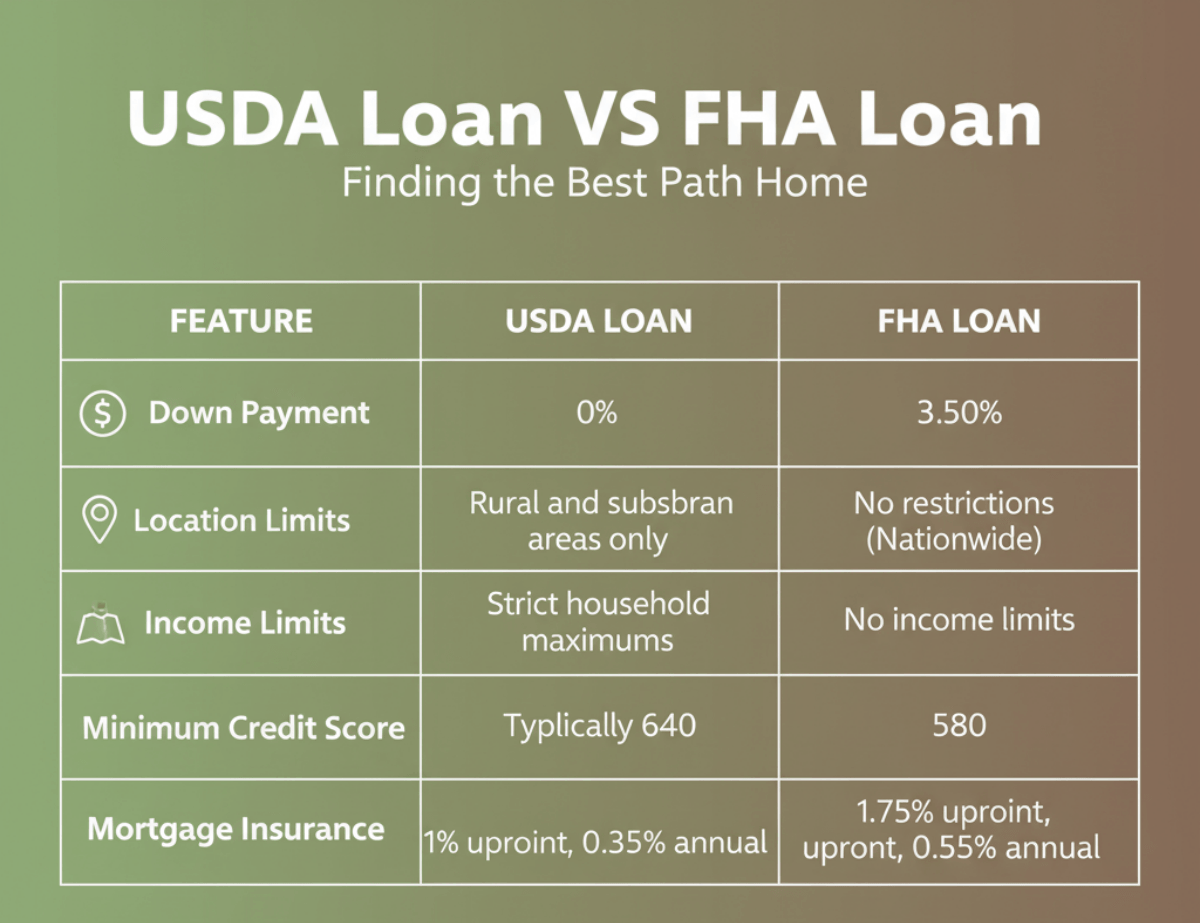

USDA Loan VS FHA Loan

When trying to buy a house with minimal cash, most people weigh the USDA against the FHA program. The biggest difference is that FHA loans are available anywhere in the country but require a 3.5% down payment, whereas USDA loans offer zero down but limit where you can live and how much you can earn. I always tell buyers: if you want to live in a suburb and meet the income caps, the agricultural department's option is cheaper overall. If you want city life or have higher earnings, FHA is the way to go.

Here is a quick breakdown to help you compare:

FAQs About USDA Loans

Q1. Are USDA loans hard to qualify for?

No, they aren't inherently difficult to secure. However, they do have strict geographic boundaries and firm household income caps. As long as you meet those two unique hurdles, the actual credit score and debt-to-income requirements are quite reasonable. A 640 score usually ensures smooth sailing.

Q2. Is USDA better than FHA?

There is no absolute winner. It depends entirely on your situation. If you are buying in an eligible suburban area and want to save cash, the USDA is better because of the zero down payment and cheaper fees. However, if you earn a high salary or prefer city living, FHA is the clear choice.

Q3. What is the maximum income for a USDA loan?

The maximum limit usually cannot exceed 115% of your specific local area's median income. For 2026, standard regions cap out at $119,850 for households of up to four people, and $158,250 for larger families. High-cost counties will feature significantly higher thresholds to match local living expenses.

Q4. What disqualifies you from a USDA loan?

Making too much money is the most common reason for denial. Other disqualifications include trying to buy a home within a major urban center, having a credit score severely below 580, or intending to use the property as an investment rental rather than your primary residence.

Q5. What is the 20% rule for USDA?

A common real estate myth says you need 20% down to avoid mortgage insurance. USDA completely ignores this rule by allowing 0% down. However, instead of private mortgage insurance (PMI), you are required to pay government guarantee fees (1% upfront and 0.35% annually) regardless of your down payment size.

Q6. Who is eligible for a USDA direct loan?

This specific tier is reserved strictly for low-to-very-low-income households who currently lack safe, sanitary housing and are completely unable to secure financing from traditional banks. The government funds these directly, often providing payment assistance subsidies that can temporarily drop the effective interest rate to 1%.

Q7. What is the USDA eligibility map?

It is an interactive online tool maintained by the agricultural department. It highlights which addresses sit in approved rural or suburban zones. Because borders shift during census updates, a house that qualified last year might not today, making this map crucial during your home search.

Conclusion

Buying a house doesn't have to drain your life savings. In my experience, the USDA loan remains one of the most powerful, underutilized tools for middle-class Americans looking to achieve homeownership without a down payment. While navigating the income caps and geographic boundaries might seem intimidating at first, the financial payoff of 100% financing and reduced mortgage insurance is absolutely worth the effort.

People Also Read

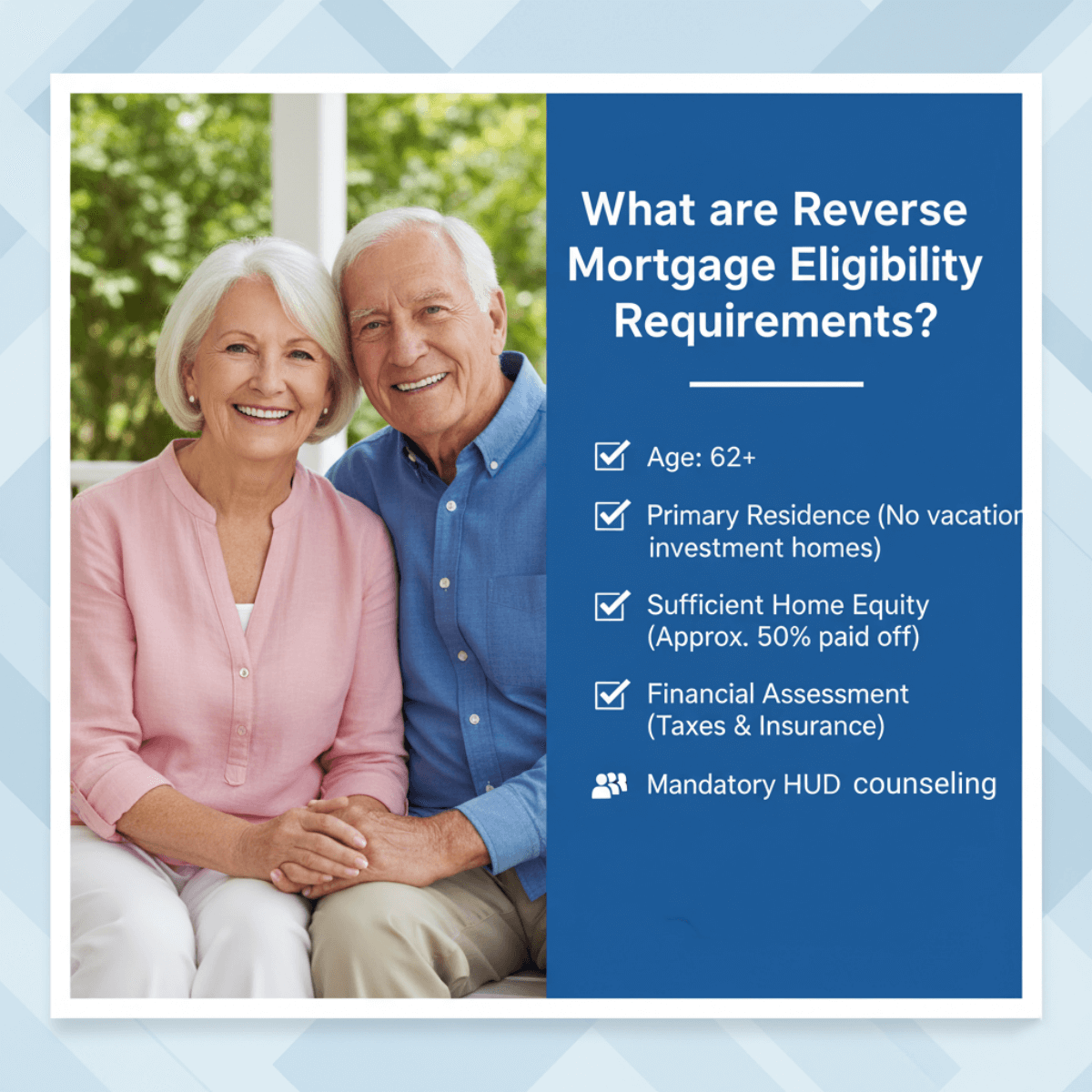

- Reverse Home Mortgage Explained: Meaning, Requirements, Example

- 1099 Form vs W2: What's the Difference? Details Here

- How to Check Mortgage Eligibility? Quick and Accurate with Sources

- What is Mortgage Eligibility Checker? Best Tool to Verify Guidelines

- Full Guide: What is a non-QM Loan? Everything to Learn

![[2026 Update] Best No Income Verification Mortgage Lenders](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69aa3ee7443901c427060cf3_best-no-income-mortgage-lenders-banner.png)

![[2026 Update] 8 Highest-Rated Reverse Mortgage Companies for You](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69a9410f689f89e0ab014f5a_best-reverse-mortgage-companies-banner.png)