Written by

Eric

Share this article

.svg)

Subscribe to updates

Let's talk about tapping into your home's value during retirement. A reverse mortgage sounds like an easy fix for cash flow, but the eligibility rules trip up a lot of people. You can't just sign a paper and get a check. Lenders have strict criteria you have to meet first, and the paperwork gets complicated fast.

Instead of getting lost in confusing guidelines, both homeowners and loan officers can actually check reverse mortgage eligibility requirements for free using smart platforms like Zeitro. Let's walk through exactly what it takes to qualify, what might get you rejected, and how to verify everything without the usual stress.

What is a Reverse Mortgage?

Generally speaking, a reverse mortgage is a loan specifically designed for older homeowners. Rather than you paying the bank every month, the lender pays you by converting a chunk of your home equity into cash. The loan balance doesn't come due until you sell the property, move out permanently, or pass away.

There isn't just one standard product out there. You generally have three types to look at:

- Home Equity Conversion Mortgages (HECMs): These are federally insured by the FHA. They are the most common and have the strictest guidelines.

- Proprietary reverse mortgages: Think of these as private loans. They are usually meant for high-value properties that exceed normal FHA limits.

- Single-purpose reverse mortgages: Offered by some state or local agencies. They cost less but restrict exactly how you use the money, like strictly for property taxes.

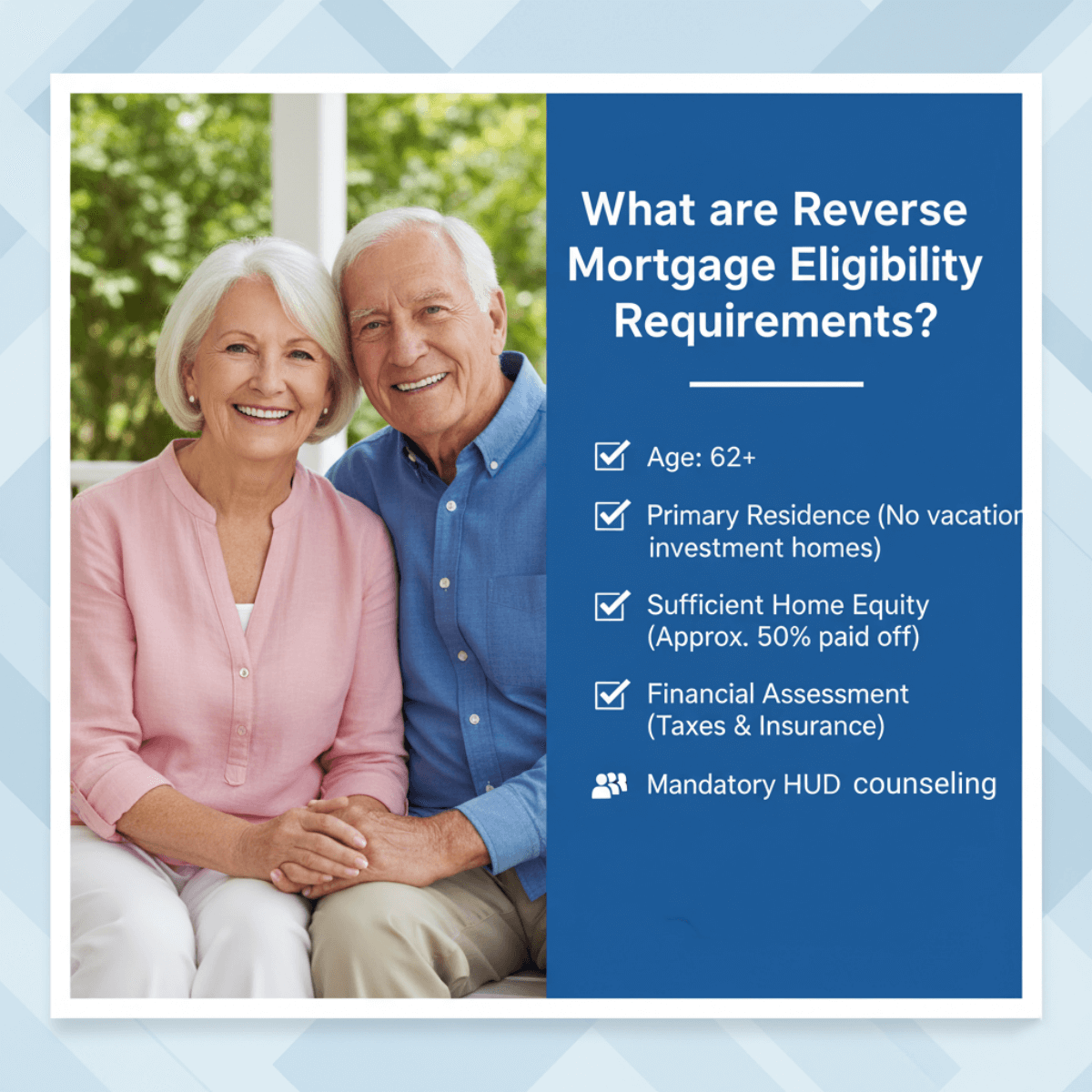

What are Reverse Mortgage Eligibility Requirements?

Assuming you qualify just because your mortgage is paid off is a huge mistake. The Federal Housing Administration sets a rigid baseline for HECMs, mostly to ensure borrowers don't end up in a worse financial spot down the road. I've seen applications stall out simply because people missed one minor detail.

Here is what you actually need to check off the list:

- Age limit: The youngest person on the title must be at least 62. No workarounds here.

- Property type restrictions: This loan only works for your primary residence. Forget about using a vacation home or an investment property you rent out.

- Sufficient equity: You either need to own the house free and clear or have paid down a massive chunk of your current mortgage, usually hitting around 50% equity.

- Passing the financial assessment: Underwriters will dig into your credit history and cash flow. You have to prove you can handle ongoing costs like property taxes, HOA fees, and homeowner's insurance.

- Mandatory counseling session: Before anything gets approved, the government requires you to meet with a HUD-approved counselor. They make sure you truly understand how this loan affects your future and your heirs. Taking this step seriously protects you from predatory lending practices.

What Disqualifies You from Getting a Reverse Mortgage?

Finding out you don't qualify after weeks of paperwork is frustrating. I always tell clients to look at the dealbreakers first. Lenders will hand out a quick rejection if you hit any of these roadblocks.

You'll likely get denied if:

- Age: You or a co-borrower hasn't hit that 62nd birthday yet.

- Equity shortage: Your existing mortgage balance is simply too high.

- Residency issues: You spend more than half the year living somewhere else.

- Financial red flags: The lender decides your income won't cover basic property taxes and insurance premiums.

- Federal debt: You have unresolved delinquent federal debt, like unpaid income taxes or defaulted student loans.

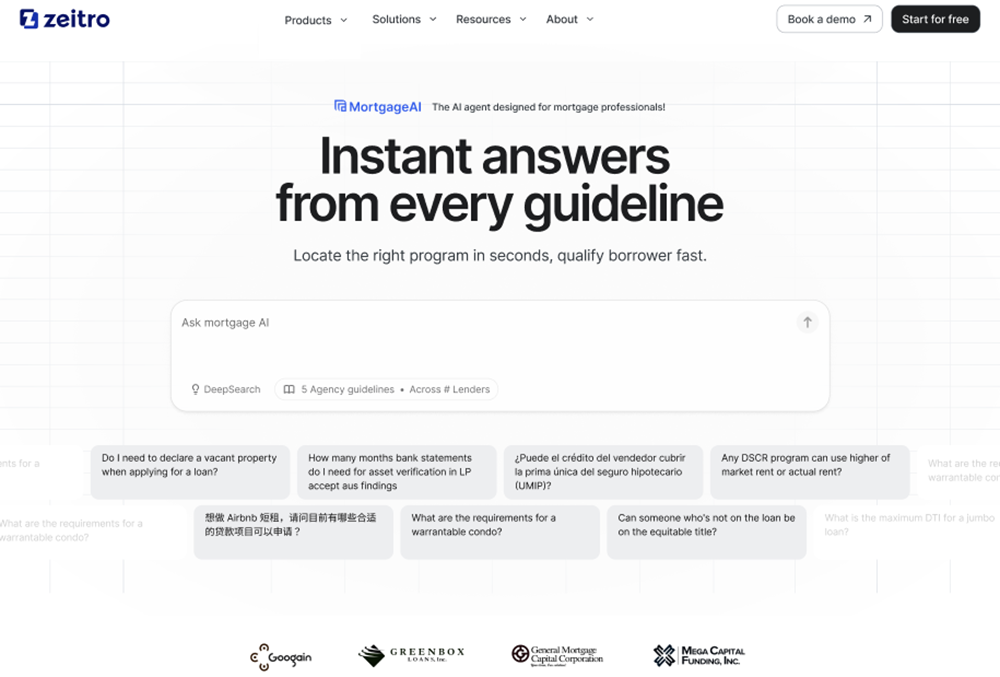

Tip: How to Accurately and Quickly Verify Reverse Mortgage Eligibility?

If you work in the mortgage industry, you already know that manually checking FHA handbooks and investor overlays is a massive time sink. Guidelines change, and trying to memorize credit and property restrictions is virtually impossible. That's why relying on old PDFs is risky.

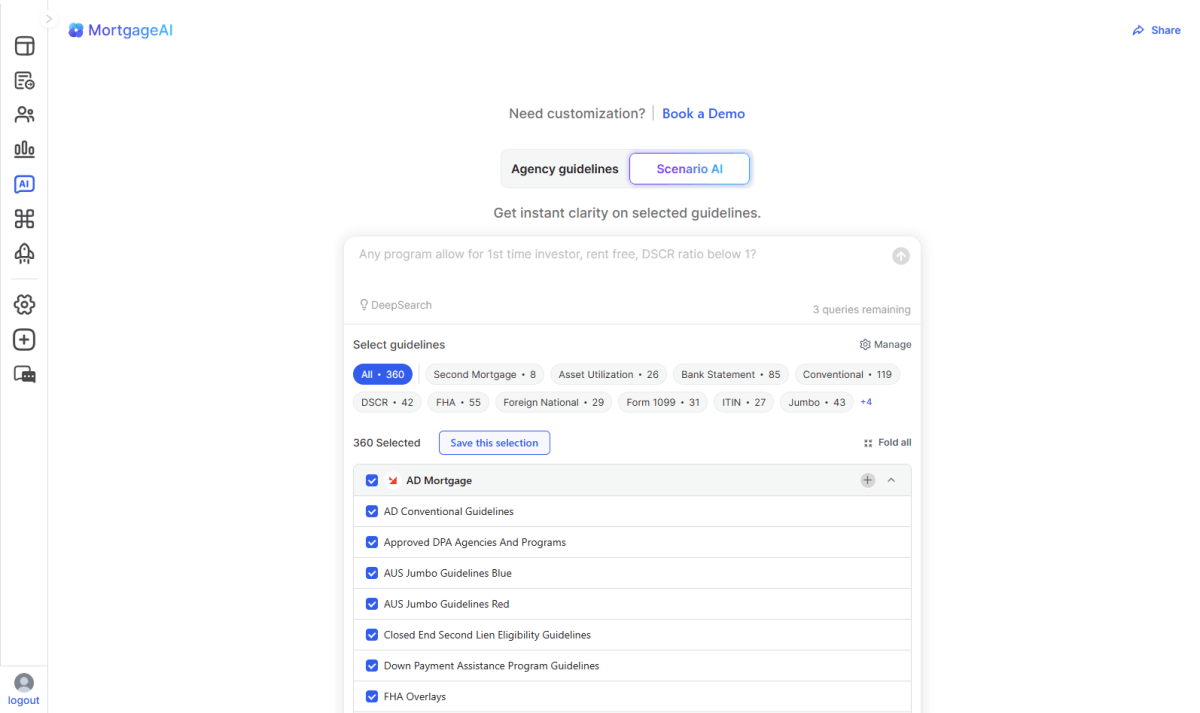

I started pointing professionals toward Zeitro Strata AI. It's an AI-native SaaS tool built purely for the mortgage space, and it essentially kills the need for manual guideline research.

Here is what makes it stand out:

- Instant answers across the board: The DeepSearch feature cross-checks over 100 investors and 300+ guidelines (covering conventional, non-QM, DSCR, and more). It turns a 30-minute manual lookup into a two-second query.

- Real source citations: It doesn't just guess. Every single answer includes a direct citation back to the original guideline, giving you the confidence that the data is 100% accurate.

- Handles messy questions: Borrowers rarely fit a perfect mold. You can type in vague scenarios or highly specific requirements in English or Chinese, and it still pulls the right rules.

- Built-in 'Explain' tool: If a specific underwriting rule still looks like gibberish, you can hit the explain function to get a plain-English breakdown of that specific text.

- Free daily access: You can actually test it out without committing. The platform gives you 3 free queries every day to run your own scenarios.

FAQs About Reverse Mortgage Eligibility

Q1. Is there a credit score or income requirement for a reverse mortgage?

There isn't a hard credit score cutoff. However, lenders run a financial assessment. They just want to ensure your cash flow can handle the ongoing property taxes and home insurance. If your credit is rough, they might require a set-aside account to cover those bills.

Q2. What is the 95% rule on a reverse mortgage?

It's a safety net. Since these are non-recourse loans, you or your heirs will never owe more than the loan balance or 95% of the home's appraised value when it's time to sell and settle the debt, whichever is lower.

Q3. What is the biggest problem with a reverse mortgage?

The upfront costs are painfully high. Between closing costs, origination fees, and compounding interest that grows because you aren't making monthly payments, your home equity gets eaten up much faster than most people expect.

Q4. What is a better alternative to a reverse mortgage?

If you have decent credit and income, a Home Equity Line of Credit (HELOC) or a standard Home Equity Loan usually costs less. Selling the house and downsizing to a cheaper place is often the smartest financial move.

Q5. What is the best age to get a reverse mortgage?

Waiting is usually better. The maximum amount you can borrow is tied directly to your life expectancy. A 75-year-old will qualify to pull out significantly more cash than a 62-year-old.

Q6. Can I lose my home with a reverse mortgage?

Absolutely. You don't have a monthly mortgage bill, but you are still strictly responsible for property taxes, insurance, and basic maintenance. Ignore those, and the lender can foreclose on the house.

Q7. Who owns your house if you have a reverse mortgage?

You do. A lot of people think the bank takes the deed, but that's a myth. You stay on the title. The lender just puts a lien on the property, exactly like they do with a regular mortgage.

Conclusion

Tapping into home equity can save a retirement plan, but the eligibility hurdles are steep. Understanding these rules upfront saves everyone a lot of wasted time.

- If you're a broker or loan officer tired of fighting through PDF guidelines, check out Zeitro. Their AI tools help pros deliver pre-qualifications 2.5 times faster and bump up loan closes by 30%. It's a massive efficiency boost.

- On the other hand, if you are a homeowner trying to figure out if you qualify, don't guess. Head to Bluerate. You can find and connect with top loan officers who use these advanced AI tools to give you accurate, free consultations and rate quotes tailored to your exact situation.

People Also Read

- Mortgage Guidelines: What Are They? How to Verify?

- Highest-Rated Reverse Mortgage Companies for You

- Best No Income Verification Mortgage Lenders

- Full Guide: What is a non-QM Loan? Everything to Learn

- How to Check Mortgage Eligibility? Quick and Accurate with Sources