Written by

Eric

Share this article

.svg)

Subscribe to updates

I still remember the sheer panic of opening my mail years ago and finding my first 1099 form. With gig work and freelancing exploding, millions of us get these tax slips every winter. But a lot of people don't really know what they are or how powerful they can be, especially when trying to buy a house. Qualifying for a mortgage without standard pay stubs feels overwhelming. Luckily, loan professionals now use tools like Zeitro Mortgage AI to verify your eligibility in seconds. Let's clear up the confusion around these forms.

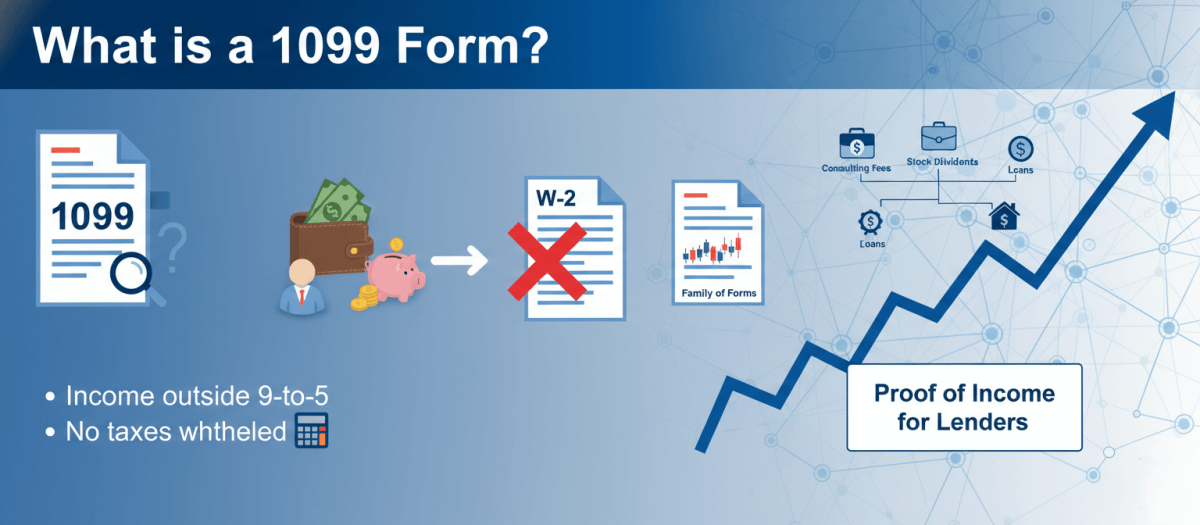

What is a 1099 Form?

Think of a 1099 form as the IRS's way of keeping tabs on cash you make outside of a standard 9-to-5 job. When I used to work a corporate gig, my boss handed me a W-2, meaning taxes were already pulled from my paycheck. A 1099 does the exact opposite. It proves you got paid, but no taxes were withheld. You get the full amount upfront, and the burden of paying income and self-employment taxes falls entirely on you later.

Honestly, it isn't just one single document either. It's an entire family of forms covering everything from consulting fees to stock dividends. While primarily a tax document, it's also a massive piece of the puzzle for proving your income to lenders if you ever want a loan.

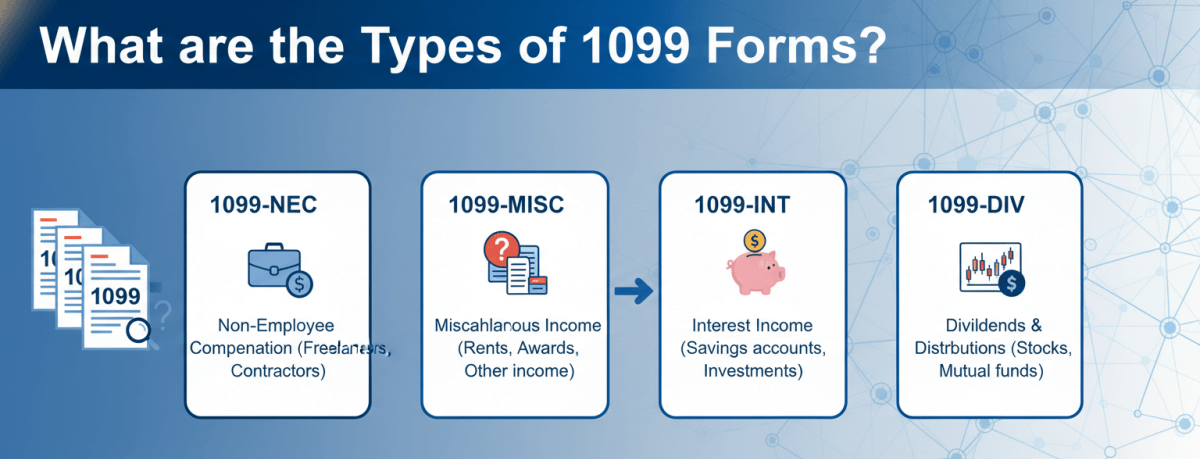

What are the Types of 1099 Forms?

Since people make money in so many different ways, the IRS created different versions of this form. I've broken down the ones you actually need to care about, whether you're freelancing, renting out a room, or trading stocks.

Form 1099-NEC

If you do any kind of freelance, contract, or gig work, the 1099-NEC (Nonemployee Compensation) is your main document. A few years back, the IRS brought this form back specifically to track freelance money. The rule is pretty straightforward: if a client pays you $600 or more during the year, they have to send you one.

I always tell my self-employed buddies to watch their mailboxes closely in late January for these. Beyond taxes, the 1099-NEC is crucial if you want to buy property. It shows underwriters exactly how much independent income you pull in. If you're trying to land a Non-QM (Non-Qualified Mortgage) loan without standard W-2s, this little piece of paper is basically your golden ticket to proving you can afford a mortgage.

Form 1099-MISC

Before the NEC form took over, freelancers used the 1099-MISC (Miscellaneous Information) for almost everything. Now, it has a more specific job. You'll usually get this if you make at least $600 from rent, prize winnings, or certain medical payments.

For example, I have a friend who rents out a condo through a property management company. Every winter, that company sends him a 1099-MISC detailing his rental revenue. If you're building a real estate portfolio or relying on rental income to qualify for a new mortgage, keeping these forms organized is non-negotiable. Lenders want to see a history of stable, reliable cash flow, and your MISC forms provide the exact paper trail they need.

Form 1099-K

Anyone selling on eBay, running an Etsy shop, or taking business payments through PayPal or Venmo will probably cross paths with the 1099-K (Payment Card and Third-Party Network Transactions).

The IRS reporting rules for this one have been a bit of a rollercoaster lately. For the 2025 tax year, the threshold is $5,000 in gross payments (no transaction minimum). It phases to $2,500 in 2026 and $600 in 2027. The prior $20,000/200 threshold was delayed according to TurboTax. One thing to watch out for: this form shows your gross volume. It includes processing fees and customer refunds. You really have to stay on top of your bookkeeping so you don't end up paying taxes on money you didn't actually keep as profit.

Form 1099-DIV & Form 1099-INT

Got a high-yield savings account or a brokerage account that pays dividends? Then expect to see these two in the mail. Form 1099-INT covers interest income of $10 or more from banks and brokerages. Form 1099-DIV handles the dividends and capital gain distributions from your investments.

I rely on these slips every year to figure out my passive income for tax season. They might seem like minor paperwork, but they matter. Some smart loan officers can actually use substantial interest and dividend earnings to help you qualify for a home loan. It shows the underwriter you have a steady, passive cash flow working in the background, making you a less risky borrower.

Form 1099-B

For the active investors and crypto traders out there, Form 1099-B (Proceeds from Broker and Barter Exchange Transactions) is the one you need to worry about. Every time you sell a stock or swap some Bitcoin, your brokerage generates this form to log your gains and losses.

What I appreciate about the 1099-B is how it separates short-term trades from long-term investments, which the IRS taxes at very different rates. It gives you the exact cost basis so filing Schedule D isn't a nightmare. Also, if you plan to use asset dissipation to qualify for a high-end mortgage, underwriters will dig deep into your 1099-B history to ensure those capital gains are consistent.

Form 1099-R

Tapping into a 401(k) or pension? You'll get Form 1099-R. This one tracks distributions from retirement plans, annuities, IRAs, and even some life insurance contracts. Fun fact: even if you just roll over an old retirement account into a new one without paying penalties, you still get a 1099-R logging the move.

I've seen plenty of retirees use the regular distributions shown on this form to qualify for a mortgage since they no longer get a paycheck. You just have to be careful with the distribution codes listed in Box 7. Those little codes tell the IRS whether your withdrawal was normal and taxable, or an early cash-out that might trigger penalties.

Other Specific 1099 Forms

Beyond the big ones, the IRS has a whole alphabet soup of niche forms. You might see a 1099-G for unemployment or state tax refunds, or a 1099-C if a lender canceled some of your debt (which, sadly, counts as taxable income). There are also forms for real estate sales (1099-S) and 529 college savings withdrawals (1099-Q). You won't see them often, but it's good to know they exist.

What is a 1099 Form Used for?

After staring at these documents year after year, I've realized they basically serve three main real-world purposes. Here's what they actually do:

- Reporting Income to the IRS: The government wants to make sure nobody is hiding off-the-books cash. When you get a 1099, the IRS gets an exact copy at the same time.

- Calculating Tax Liability: Since you haven't paid taxes on this money yet, you and your accountant need these numbers to figure out what you owe in federal, state, and self-employment taxes.

- Mortgage Qualification: This is huge. If you don't have W-2s, these forms act as hard proof of your income, letting you qualify for specialized home loans designed just for self-employed buyers.

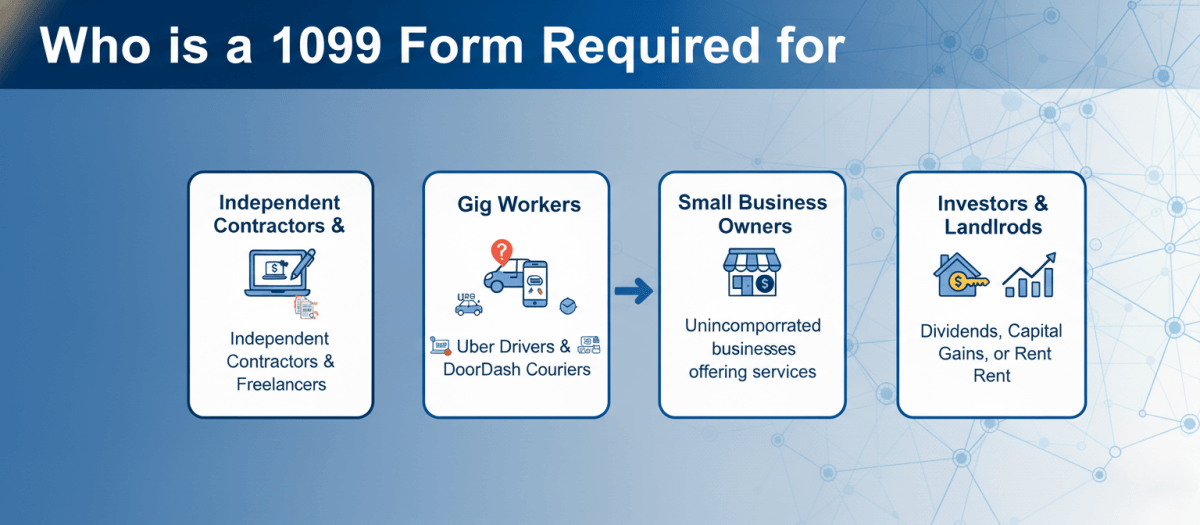

Who is a 1099 Form Required for?

The group of people receiving these forms is massive. Essentially, if you earn money outside of a traditional boss-and-employee setup, you're on the list.

- Independent Contractors & Freelancers: Writers, designers, and consultants.

- Gig Workers: Uber drivers and DoorDash couriers.

- Small Business Owners: Anyone running an unincorporated business offering services to others.

- Investors & Landlords: People earning dividends, capital gains, or rent.

The golden rule here is the $600 threshold. If a company pays you more than $600 for a service over the calendar year, the legal burden is on them (the payor) to issue this paperwork to you (the payee).

How to Get a 1099 Form?

Here's the good news: you don't actually have to apply for one. The company or platform that paid you is required to send it. They usually mail a paper copy or shoot you an email with a secure download link early in the year. If something gets lost in the mail, you can pull a Wage and Income Transcript straight from the IRS website.

Once you've got your forms, what's next? If you want to use that freelance income to buy a house, things get a bit more complicated than a standard loan. I highly suggest checking out Bluerate to chat with a local, professional Loan Officer for free. They know exactly how to leverage your 1099s to find a lender that fits your situation.

When are 1099s Issued?

Timing matters a lot when you're trying to file taxes on time. Legally, payers have to send out most of these forms, like the NEC and MISC, by January 31st. If that date lands on a weekend, the deadline bumps to the next business day.

But don't stress if your mailbox is empty on February 1st. Forms related to investments, like the 1099-B from your broker, usually get an extension and might not show up until mid-February. My personal rule? I just wait until late February before I even touch my tax return to make sure nothing is missing. You'll need all of them well before the April 15th filing deadline.

Tip: How to Verify 1099 Form Eligibility?

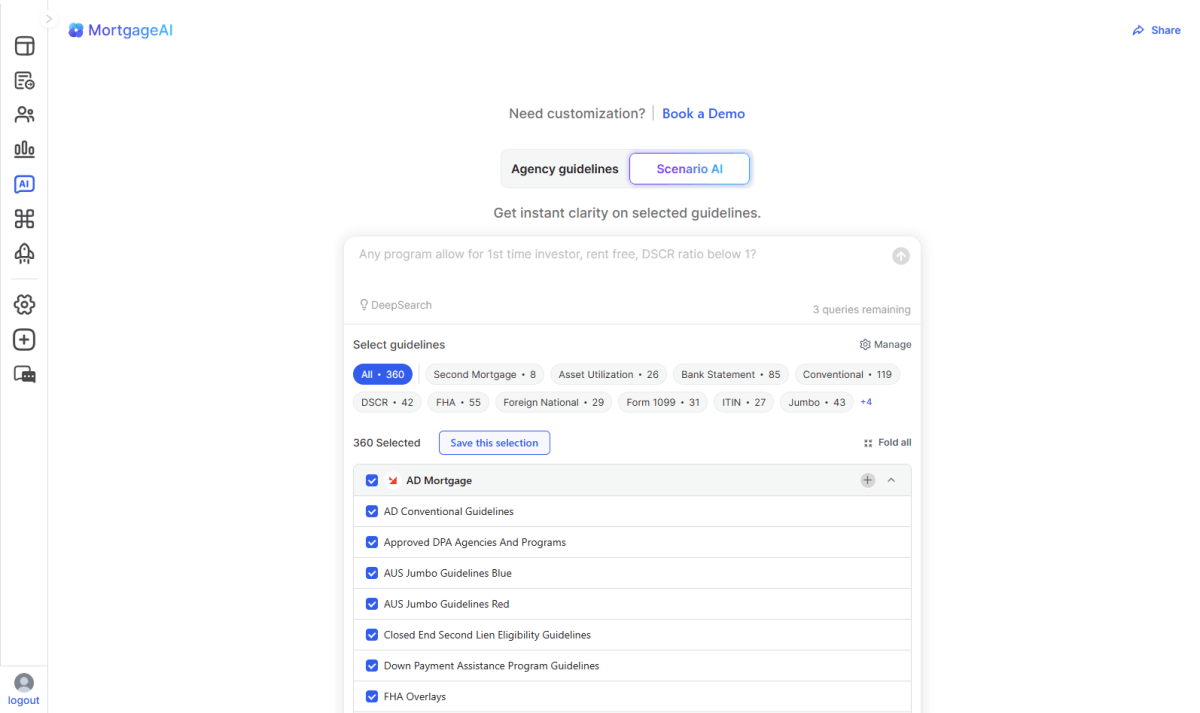

If you're a Loan Officer, Processor, or Underwriter, you already know the pain of verifying a self-employed borrower's income. Flipping through hundreds of pages of Non-QM guidelines to figure out if a lender accepts a 1-year or 2-year 1099 history takes way too much time. This is exactly where Zeitro Mortgage AI comes in.

It's an AI-powered Mortgage Guideline Assistant built specifically for QM and Non-QM loans. It instantly searches over 300 guidelines (including 31 distinct 1099 Form Mortgage Guidelines) from top lenders like AD Mortgage, CMG Financial, and Freedom Mortgage.

Here's a quick look at why it's so useful:

- Instant Citations: It gives you precise answers in seconds, backed by clickable source links so you know the info is legit.

- All-Scenario Support: Ask broad "what is" questions or run tight prequalify scenarios in both English and Chinese.

- DeepSearch & Explain: Filter by specific lender guidelines or ask it to break down complex underwriting blind spots.

- Efficiency Boost: It cuts out manual reading, integrates smoothly with your LOS, and speeds up the whole loan process.

- Great Price: It's faster than the competition and starts at just $8/month (plus you get 3 free queries a day to test it out).

FAQs About the 1099 Form

Q1. What is the difference between a 1099 and W-2?

A W-2 is for regular employees. The company takes out taxes before you even see your paycheck. A 1099 is for contractors. You get the full amount paid directly to you, which means you have to handle calculating and paying your own income and self-employment taxes later.

Q2. Does a 1099 mean I have to pay taxes?

Almost always, yes. Since the company that paid you didn't withhold anything, you have to report this income. Depending on how much profit you actually made after deducting your business expenses, you'll owe regular income tax plus the self-employment tax.

Q3. How much tax will you pay on a 1099?

It really depends on your tax bracket and your write-offs. Generally, independent contractors pay a 15.3% self-employment tax (for Medicare and Social Security) on top of their normal income tax rate. But remember, you get to deduct business expenses like internet, software, and mileage to lower that bill.

Q4. What happens if I don't file a 1099 on taxes?

I wouldn't risk it. The IRS already has a copy of the form. If your tax return doesn't match their system, it triggers an automatic CP2000 notice. That usually leads to penalties, extra interest on what you owe, or a full-blown audit.

Q5. Do I need to file a 1099 form?

If you're the one who got paid, you just use the numbers on the form to fill out your Schedule C. You don't mail the paper itself. If you're a business owner who paid a contractor over $600, then yes, you must file it with the IRS and send the contractor a copy.

Conclusion

At the end of the day, a 1099 form is more than just an annoying chore during tax season. It's actual proof of your income and financial hustle. Whether you're trying to calculate your business deductions or using that cash flow to prove you can afford a new house, keeping track of these documents is a must.

For the mortgage pros out there tired of hunting through Non-QM guidelines manually, definitely give Zeitro Mortgage AI a try to speed up your approvals. And if you're a self-employed borrower trying to figure out how to buy a home with freelance income, don't do it alone. Jump onto Bluerate AI Agent to find a local Loan Officer who can make the process smooth and painless.

People Also Read

- Mortgage Guidelines: What Are They? How to Verify?

- What Does a Loan Officer Do? Duties, Pros, Cons, and Outlook

- Best DSCR Loan Lenders: Which to Choose from?

- 8 Best Non-QM Mortgage Lenders: Which to Choose?

- Refinance Meaning: What Refinancing a Mortgage Really Means